R&D Capitalization Tracking Guide: 5 Steps to Stay Audit Ready in the US

Master R&D capitalization in 5 steps and stay audit-ready under US standards.

After the 2022 tax reform, your approach to R&D cost tracking likely shifted. You now need cleaner records, clearer audit trails, and stronger alignment between engineering data and financial reporting

R&D capitalization tracking impacts how you plan, report, and defend your expenses. In this article, you’ll get a practical, 5-step guide to keep your records clean and audit-ready.

But first, let’s clarify what R&D capitalization actually means.

What Is R&D Capitalization?

R&D capitalization means recording qualifying research and development costs as long-term assets instead of immediate expenses. As you likely know, this shifts how those costs appear on your balance sheet and how deductions are timed on your tax return.

While Section 174 now requires this treatment for foreign R&D, GAAP and IFRS apply different thresholds based on purpose and jurisdiction (but more on that shortly).

The first step is at least trying to capitalize your R&D costs.

Unfortunately, according to a 2023 study by Campbell and colleagues, only 29% of companies capitalize any R&D costs in a given year. And when they do, it averages about 7% of total spend.

We’ll help you escape this statistic by helping you understand more about R&D capitalization and its rules.

So, let’s see how the capitalization of R&D costs compares to expensing.

R&D Capitalization vs. Expense

Expensing deducts R&D costs in the same year they occur. Capitalization spreads those costs over time. This difference matters for your audit trail, your reported earnings, and your compliance with R&D capitalization GAAP and Section 174.

Misclassifying costs or applying the wrong treatment can throw off everything from tax filings to internal forecasts.

You probably already track some R&D in spreadsheets or project tools, but that alone won’t meet audit expectations. Clean time categorization, traceable logs, and aligned standards take more structure.

Moving on, let’s talk about the benefits of R&D capitalization.

Benefits of R&D Capitalization

Choosing to capitalize qualifying R&D costs gives you more than a different line on a financial report. It reshapes how internal teams work together and how external reviewers see your operations.

Here are the key benefits of building a clear R&D capitalization tracking process:

- Strengthens your balance sheet by converting costs into long-term assets.

- Creates a clearer view of how innovation efforts contribute to future value.

- Enhances audit readiness through structured records that connect engineering data to financial reporting.

- Improves claim potential for tax incentives such as Canada’s SR&ED or the U.S. R&D Tax Credit, while supporting compliance with section 174 R&D capitalization rules.

- Helps engineering and finance align on R&D timing, cost classification, and project scope.

- Builds stronger claims. In Canada’s SR&ED program, over 90% of submissions accepted as filed had strong documentation.

However, as I pointed out above, less than a third of companies file for R&D cost capitalization in the first place. This doesn’t happen in every niche, though.

According to the Armanino LLP survey, 69% of top public SaaS companies now capitalize software R&D costs, up from 62% in 2017.

One reason can be that SaaS companies rely heavily on continuous product development as a core driver of valuation.Capitalizing R&D allows them to smooth out expenses, report stronger short-term margins, and better align development costs with the revenue those features will generate over time.

Another factor is investor pressure: in SaaS, recurring revenue multiples are tightly tied to growth efficiency. So, presenting cleaner profitability metrics gives these firms a strategic edge when raising capital or competing for market share.

If you want to start R&D cost capitalization, too, you need to understand the rules that govern this practice. So, let’s break down how those rules differ across tax and accounting standards.

R&D Capitalization Rules

R&D costs follow two main rulebooks: GAAP for your financials and Section 174 for your tax filings. Each framework applies different rules for expensing and capitalization.

Here are the key areas where R&D expense capitalization comes into play, and where your audit trail needs to stay aligned.

R&D Capitalization GAAP

Under Generally Accepted Accounting Principles (GAAP), most research and development costs must be expensed when incurred. This reflects the uncertainty in predicting whether early-stage R&D will yield future economic benefits. As a result, GAAP tends to favor conservatism over speculation when classifying R&D costs.

That said, there are clear exceptions.

In specific cases, you can capitalize costs if they meet certain criteria. These carve-outs are narrowly defined, but they matter when building a compliant and defensible R&D capitalization tracking system.

General Rule

- R&D costs are expensed as incurred (ASC 730).

- Applies across most industries, including software, pharma, biotech, automotive, etc.

- Rationale: High uncertainty of outcomes makes capitalization unreliable.

Exceptions to the Rule

While most R&D costs fall under the expense category, certain types of projects qualify for capitalization. Here are the most common GAAP exceptions:

Software Development

If you’re building software, treatment depends on purpose and stage of development.

- Internal use (ASC 350-40): Capitalize once the project enters the application development stage. Costs during planning and post-implementation (such as training and maintenance) are expensed.

- For sale or lease (ASC 985-20): Expense all costs before technical feasibility. Once that milestone is met, capitalize until the product is released.

Entertainment and Creative Content

GAAP allows capitalization of direct production costs for media, entertainment, and creative projects (ASC 926, 920, 928). Marketing, overhead, and promotional efforts must still be expensed.

Extractive Industries

For companies involved in natural resource exploration, ASC 932 permits capitalization of successful efforts. Unsuccessful attempts, such as dry wells, must be expensed.

Patents and Intangibles

If you're incurring costs related to patents, ASC 350 allows capitalization of legal fees and registration costs. R&D activity that precedes invention is still expensed.

Prototypes and Fixed Assets

Prototypes built strictly for testing or internal research must be expensed under ASC 730.

However, if a prototype evolves into a tangible asset with an alternative future use (for example, equipment or facilities that will be deployed in commercial production) it falls under ASC 360. That means it can be capitalized as property, plant, and equipment.

The key distinction is whether the prototype remains experimental or becomes a revenue-generating asset.

Practical Considerations

If you're working with mixed-use equipment or developing both internal tools and commercial software, you’ll likely need to document how each cost is allocated. GAAP expects you to support those decisions with clear reasoning.

This makes R&D capitalization journal entry documentation necessary for audit preparation. Without supporting evidence, costs default to expense treatment, even if they qualify for capitalization.

Sec 174 R&D Capitalization

Section 174 governs how you handle R&D expenses for federal tax purposes.

From 2022 through 2024, companies were required to capitalize and amortize all R&D expenditures, which meant no immediate deduction was available. That created a sharp divergence from GAAP reporting and forced teams to spread deductions over time.

As of July 2025, new legislation (IRC §174A) under the Congress-approved Big Beautiful Bill restored immediate expensing for domestic R&E (Research & Experimental)* for tax years beginning after December 31, 2024.

*Note: R&E (Research & Experimental) = R&D (Research & Development), but the terms are used in different contexts. GAAP/IFRS use R&D (Research & Development) terminology. The U.S. tax code (Section 174, Section 41) uses R&E (Research & Experimental) expenditures. They’re referring to essentially the same types of activities, but the IRS deliberately uses R&E in the Internal Revenue Code to avoid confusion with GAAP definitions.

However, foreign R&E still must be capitalized and amortized over 15 years. Companies may also deduct remaining unamortized domestic amounts from 2022–2024 in 2025 (or spread them over 2025–2026), depending on their election.

This is why many finance teams now keep two sets of books:

- GAAP (ASC 730): Most R&D is expensed when incurred, unless another standard applies (e.g., internal-use software under ASC 350-40).

- Tax (Sec. 174): Domestic R&D may now be expensed again, but foreign R&D must still be amortized.

Here’s a quick way to think about it:

- GAAP (for investors): “We took the full hit this year.”

- Section 174 (for the IRS): “We’re deducting this cost either all at once (domestic) or stretched over 15 years (foreign).”

These rules apply to what the IRS defines as Specified Research or Experimental (SRE) expenditures. That includes:

- Wages for technical staff tied to software or product development.

- Supplies and contract research linked to new features, capabilities, or architecture.

- Costs involving uncertainty in design or process outcomes.

Excluded activities are just as important to track. These include:

- Quality control and routine testing.

- Efficiency studies and consumer research.

- Advertising and promotional work.

- Acquiring patents, models, or externally developed IP.

Getting this classification right is critical, since mislabeling SRE vs. non-SRE expenses can affect both deductions and audit outcomes.

Section 174 is no longer a blanket capitalization rule. However, it still requires careful separation of domestic vs. foreign R&E, and clean documentation to support how costs are treated for both GAAP and tax purposes.

That’s why automation matters.

Chrono Platform helps you with better cost management by automating R&D capitalization tracking and maintaining clean separation between technical and non-technical effort, without the need to rebuild cost trails manually.

IFRS R&D Capitalization

If your SaaS company operates foreign subsidiaries or prepares consolidated financials under IFRS, you’re likely working with a different set of R&D rules than what GAAP or Section 174 require. The IFRS approach usually leads to more R&D capitalization than U.S. standards, which makes cross-border alignment more complex.

Under IAS 38, the research phase must be expensed as incurred. This is consistent with GAAP. But the key difference comes in the development phase, where IFRS permits capitalization if strict criteria are met. This includes:

- Demonstrating the technical feasibility of completing the asset.

- Proving the intention and ability to use or sell it.

- Showing that the asset will generate probable future economic benefits.

- Having sufficient technical, financial, and other resources to complete the project.

- Being able to reliably measure development costs.

If your foreign entity meets all six requirements, development costs must be capitalized.

That includes salaries, contractor spend, and other directly attributable inputs. The challenge is that IFRS doesn’t limit this to software or internal tools. Instead, it applies to all R&D investments, from platforms to scientific advances.

Note: For cloud software you use (SaaS), IFRIC clarified in 2021 that most configuration/customization costs are expensed, unless they create a separable intangible or a prepaid service.

You also need to monitor in-process R&D acquired through business combinations.

IFRS 3 requires you to recognize those intangible assets at fair value on day one, even if the project hasn’t reached feasibility. That triggers both recognition and impairment testing obligations because these assets are not yet available for use (IAS 36).

The bottom line is that IFRS introduces more opportunities and responsibilities for R&D capitalization tracking, especially across M&A, multi-entity consolidations, and intangible asset reviews. That means more audit prep, more valuation diligence, and a tighter process to keep your IFRS and U.S. tax records in sync.

That’s why next, we’ll cover how to build audit-ready systems that keep those records aligned.

5-Step Guide to R&D Capitalization

Section 174 and its newest amendments changed how you handle R&D costs, and the IRS is already asking companies to prove their treatment. The challenge is to build a system that accurately reflects how work is actually done across finance and engineering. Here are the five steps that help you build a defensible, real-time ledger.

1. Centralize R&D Project Tracking

Fragmented data sources are a major risk in any R&D audit. Engineering might be logging work in Jira or GitHub, while finance is updating spreadsheets after the fact. That delay, and the lack of context behind each cost, can easily lead to misstatements.

Instead of retroactively chasing receipts, you need project-level tracking that connects work to cost attribution in real time. The truth is, most spreadsheets fall short, especially when you’re trying to map costs to capitalization criteria under both GAAP and Section 174.

Chrono helps you connect calendars, code repositories, project management tools, and ERPs so you get a clean audit trail without manual cleanup. Time entries, ticket data, and cost inputs can be tied directly to the asset or initiative they support.

Because Chrono uses AI agents to pull attribution data across sources, you reduce dependency on manual tagging. That means less rework when auditors ask for supporting schedules.

You likely already have a rough system for tracking costs, but unless that system aligns with audit expectations and keeps pace with engineering activity, it becomes a liability. Investing in AI-powered R&D capitalization tracking is the first step to fixing it.

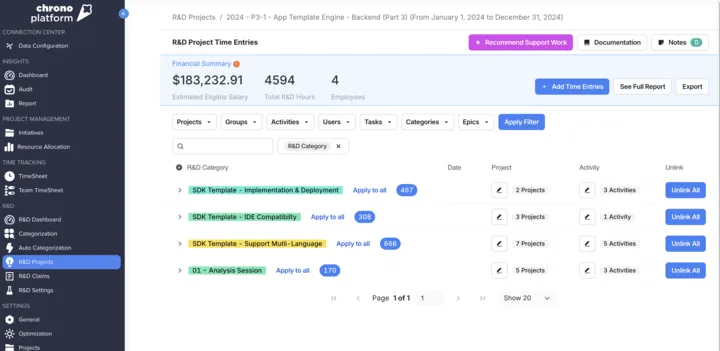

2. Segment Research vs. Development Costs

Capitalization starts with classification.

IFRS requires you to expense research and capitalize qualifying development once all six IAS 38 criteria are proven. US GAAP generally expenses both research and development under ASC 730; capitalization is limited to specific standards outside ASC 730 that we explained above (e.g., ASC 350-40 for internal-use software after the application-development stage; ASC 985-20 for software to be sold after technical feasibility).

Section 174, however, requires capitalization across the board for foreign expenses, though it allows expensing for domestic R&D.

This makes the research vs. development split and the domestic vs. foreign split operationally critical.

In practice, separating the two categories is harder than it sounds.

Labels in Jira or Asana rarely align with capitalization criteria. Also, project names usually carry over from earlier phases and can blur intent. Without structured classification logic, those gray areas turn into misreported costs.

Chrono applies AI to detect phase shifts and automatically reclassify costs. For example, if a product moves from feasibility to technical development, the AI flags the cost center and adjusts the categorization behind the scenes. No need to re-code the entire data set mid-quarter.

And with §174 rules changing again in 2025, Chrono’s reclassification capability matters more than ever.

Clear segmentation also helps with audit readiness. When an auditor asks how you treated an ambiguous project, you’ll have not only the time logs but also the decision trail that supports your treatment.

And if you’re preparing for a potential R&D capitalization repeal or update in tax treatment, having that split already built in lets you adjust without rebuilding schedules from scratch.

3. Align with Accounting Standards Early

It’s not enough to document R&D activity after the fact. To avoid rework and costly adjustments, map your project data to accounting standards as the work unfolds. That means applying the right treatment based on GAAP, Section 174, or IFRS well before tax prep or year-end close.

The challenge isn’t just about knowing the rules.

In fast-moving environments, project scope and stage shift quickly.

A feature that starts as exploratory can become development-ready in the same sprint. Without early alignment, your teams risk capturing data under the wrong framework and forcing finance to backtrack and reclassify costs later.

That’s why Chrono is built to surface accounting logic at the point of entry.

Chrono’s platform can flag which treatment applies as work progresses, so engineers, PMs, and finance stay synced across each project’s lifecycle. By the time you reach your close process, most of the accounting logic is already in place.

This kind of real-time mapping reduces the chance of misclassification and minimizes compliance risk. More importantly, it removes the last-minute scramble to justify treatment choices in front of auditors.

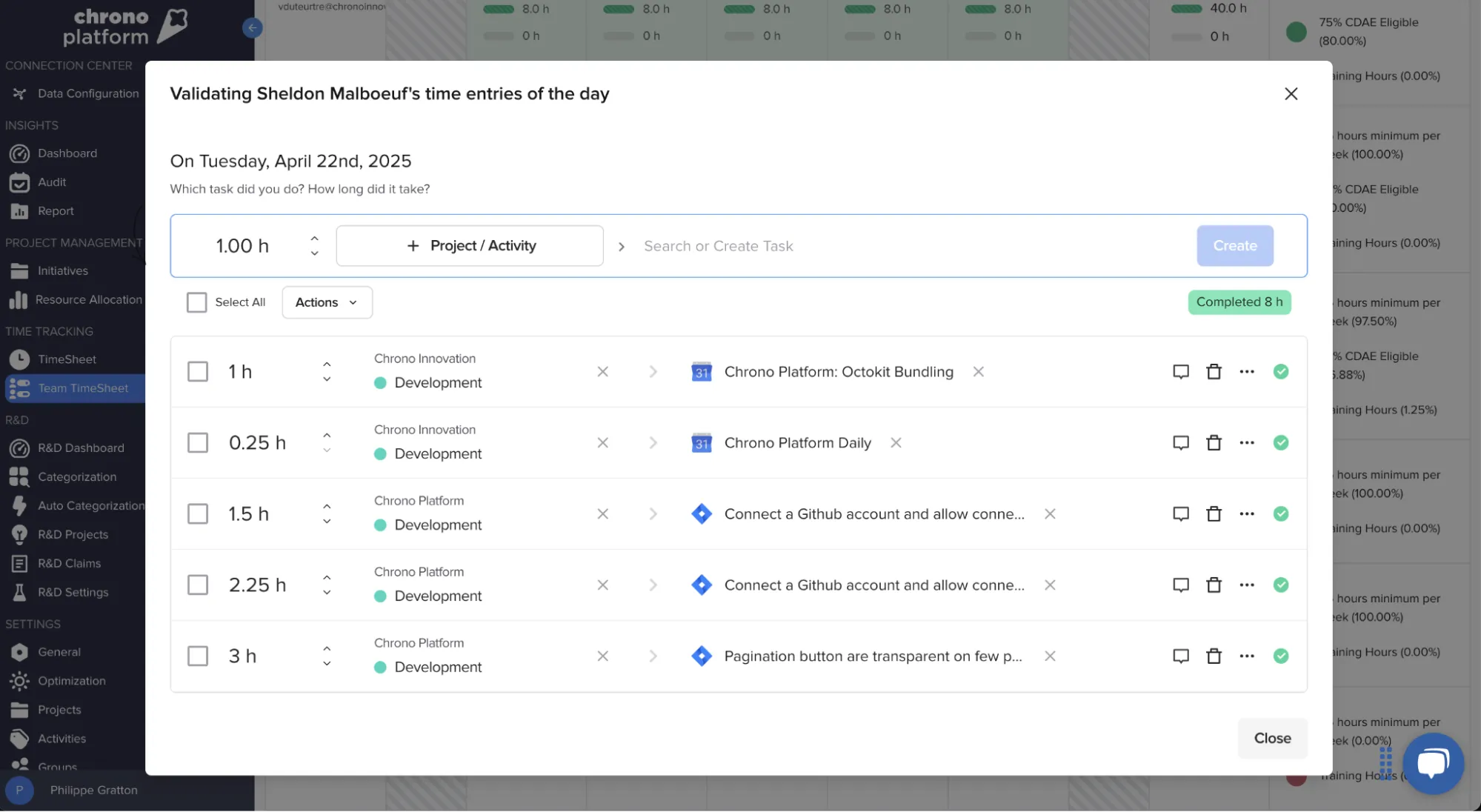

4. Maintain Audit Ready Documentation

One of the biggest risks during audit season is having gaps in supporting detail, and it’s not just about totals. Reviewers expect to see how costs link to time spent, engineering intent, and technical output. That means you need clean records for wages, time attribution, and project-level activity.

Pulling that data retroactively, especially from fragmented tools such as Jira, Excel, and payroll systems, can be slow and error-prone. Notes get buried, sprint logs get overwritten, and time entries lose context. Reconstructing the full picture is possible, but typically messy.

Chrono solves this by linking technical documentation and time tracking directly to accounting categories.

Its AI agents automatically assign time entries to the right project, track changes over time, and compile payroll records that align with capitalization rules.

Even meeting transcripts and code commits can be tagged and archived to support R&D claims.

The benefit isn’t just audit protection. This type of structured documentation makes your close process faster, your tax position more defensible, and your internal reporting cleaner. If you’re working under Section 174, these trails are important.

With audit-ready data flowing from your day-to-day tools, you avoid cleanup work and reduce your exposure when questions come up later.

5. Review Regularly with Finance & Tax Teams

Even the best-built tracking systems need routine checks. R&D capitalization rules don’t sit still because guidance shifts, interpretations evolve, and what was compliant last year may need adjustment this quarter. That’s why quarterly reviews with your finance and tax partners are important.

When you align early and regularly, you catch classification errors before they hit your year-end reports. You avoid struggling to retroactively fix journal entries. Plus, you stay ahead of changing rules around capitalization of R&D costs, especially under Section 174 or IFRS updates that quietly shift the line between capitalizable and expensable spend.

Set a fixed cadence, ideally every quarter, to review active projects, validate how costs are categorized, and update documentation standards. These sessions should include space to evaluate new initiatives, assess which tax credits apply, and recalibrate for any legislative changes (including pending reform or potential R&D capitalization repeal efforts).

As we mentioned above, Chrono can simplify this review process by letting you re-categorize time, payroll, and contract data with a few clicks. Its AI agents automatically adjust classification logic based on rule changes, so your compliance stays current without adding overhead. Also, when finance and engineering see the same audit-ready view, decisions move faster with less risk.

Examples of R&D Capitalization

To make capitalization rules more concrete, here’s a simplified walkthrough based on a common scenario in software R&D capitalization. Let’s say you invest $150,000 to build an internal-use platform. The project is complete and live, with a commercial life of six years and a $30,000 residual value. Using straight-line amortization, you expense $20,000 per year until the asset reaches the end of its useful life.

In your R&D capitalization journal entry, you’d credit cash or payroll expense and debit a long-term intangible asset at the time of capitalization. Each year, you’d record amortization expense and reduce the carrying value of the asset.

Chrono’s AI can help you automate both the classification and calculation steps behind this process, which reduces error risk and frees your team from time-consuming manual work.

Get Ahead of R&D Compliance Without the Headaches

When your R&D capitalization tracking is accurate, then your financial reporting holds up under pressure, your tax strategy stays defensible, and audits run smoother.

With changing rules across important legislation, manual processes break down fast.

That’s where Chrono comes in.

From R&D capitalization tracking to audit-ready documentation, our AI-powered platform simplifies the hard parts automatically.

You get real-time visibility into R&D activity, smart categorizations across teams, and support for complex rules such as Section 174 amortization software. The result is better books, faster closes, and no surprises during audit or tax season.

Sign up for Chrono and take the complexity out of compliance before it costs you.

FAQs

How is R&D capitalized?

Under GAAP, most R&D costs are expensed, but some development costs, such as software after feasibility, can be capitalized. Section 174 requires capitalization for federal tax, amortized over 15 years for foreign R&E; under the 2025 Big Beautiful Bill, Section 174 allows expensing of domestic R&E. IFRS allows capitalization if strict development-phase criteria are met.

How to track R&D?

You need structured systems to track time, costs, and technical activities by project phase. That includes payroll, contractor logs, and tool-level integrations. Chrono Platform automates this using AI to classify, document, and sync data across engineering and finance without manual backtracking.

Can R&D be capitalized in IFRS?

Yes, but only during the development phase, and only if specific conditions are met. These include proving technical feasibility, commercial intent, available resources, and future economic benefit. Research costs must still be expensed.

How many years are R&D expenses capitalized over?

For Section 174, 15 years for foreign R&D. For GAAP or IFRS, amortization depends on the asset’s useful life. There’s no general timeline.

Is capitalization of R&D optional?

Under Section 174, it’s mandatory for foreign R&E. Under GAAP or IFRS, it depends on whether the costs meet the capitalization criteria. Otherwise, they must be expensed.

Can you claim R&D on capitalized costs?

Businesses are allowed to claim R&D tax relief on certain capital costs connected to their research and development work. While many R&D expenses are recorded directly as costs, some (especially those tied to equipment or assets used in R&D) are handled differently. Instead of deducting them all at once, these costs can be treated as long-term assets on the balance sheet and written off gradually through depreciation.